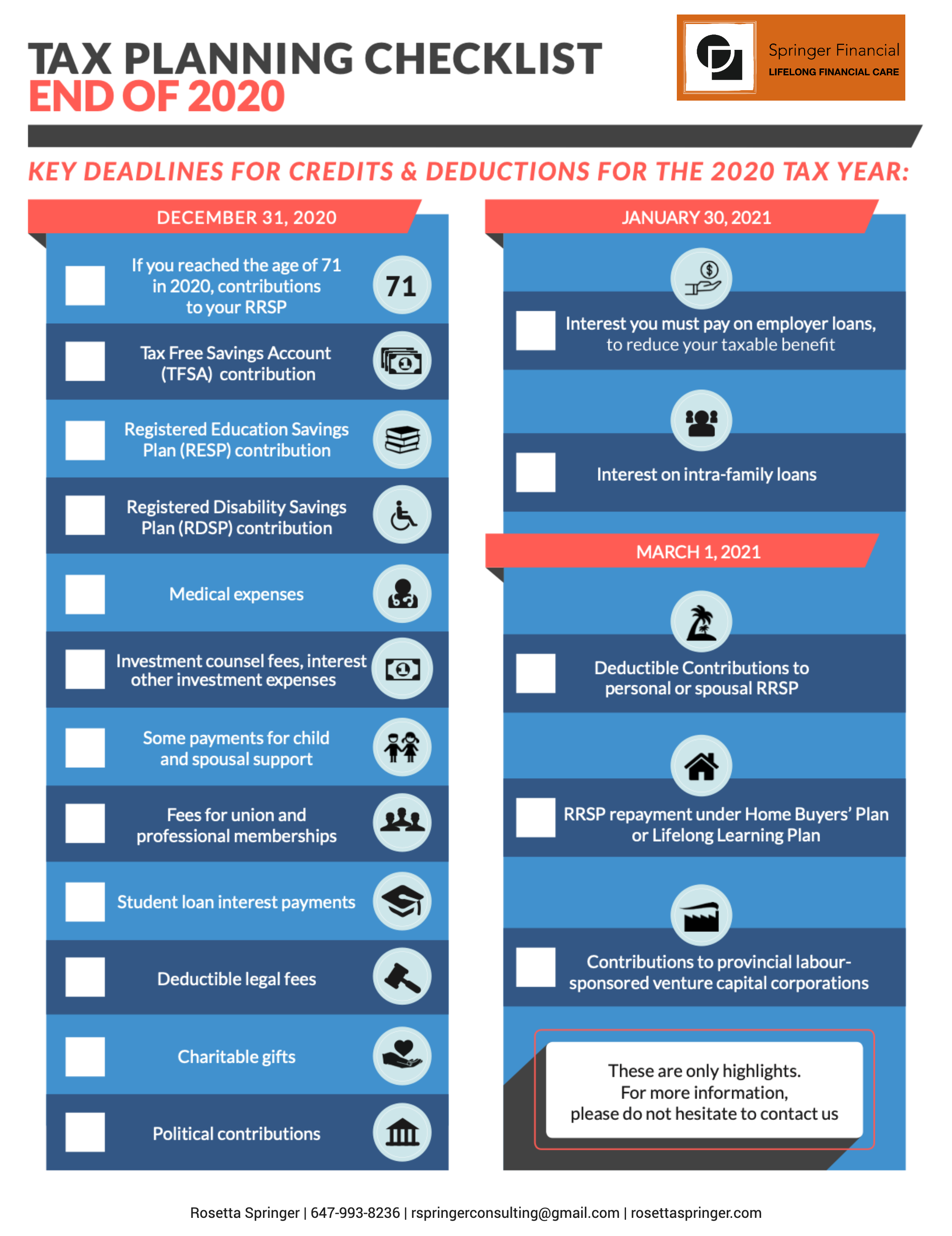

Personal Tax Planning Tips – End of 2020 Tax Year

2020 Only, Blog, Charitable Gifting, Coronavirus, Coronavirus - Associates, Coronavirus - Practice Owners, Coronavirus - Retired, Coronavirus - Retiring, Coronavirus - Students, disability, Disability Insurance, Family, financial advice, Financial Planning, health benefits, pension plan, RDSP, Registered Education Savings Plan, RRSP, tax, Tax Free Savings AccountRosetta Springer